Today we launch Homeless Link’s Support to End Homelessness 2024: review of services addressing single homelessness in England (formerly the Annual Review). Cate Standing-Tattersall, our Research Officer, unpacks key findings from the seventeenth edition of the report.

Since 2008, we have tracked the sector’s shape, size and challenges, and the circumstances of people accessing homelessness support. The research aims to help service providers, commissioners, policy makers, and local authorities respond to the needs of people experiencing homelessness.

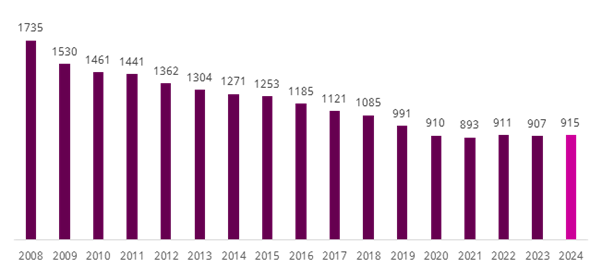

Shape of the sector: rising homelessness and reduced capacity

The report shows that there are 915 accommodation projects across England, a decrease of 47% since the research series began. There are 33,249 bedspaces available, a 43% decline since 2008, and 173 day centres currently operating - 7% fewer than in 2008. The sector has contracted sharply over the past 17 years and recent stabilisation, following the introduction of RSI and other grant funding sources, has only stemmed the decline.

At the same time, all forms of homelessness are increasing: the last year has seen statutory homelessness increase by 4%, rough sleeping by 20%, and temporary accommodation by 12%. Demand is rising rapidly and rather than receiving investment to grow, the sector is reducing in capacity.

Number of accommodation providers, 2008 - 2024

With 39% of people currently accommodated waiting to move into more secure, sustainable housing due to lack of social housing or private rented properties, the effects of the affordable housing collapse on the homelessness system are ever clearer. People are trapped, unable to move on, while people on our streets or experiencing other forms of homelessness cannot access the support they need, compounding the pressure on an already stretched system.

The last line of defence: supporting increased complex need

Alongside demand, the complexity and level of need has increased. 74% of accommodation projects and 82% of day centres reported a rise in people presenting with multiple needs. This coupled with insufficient funding has meant increased instances where providers are unable to meet need: 81% of accommodation projects had to turn someone away because their needs were too high or complex.

While we know that people experiencing homelessness suffer from worse mental health than the general population, the 2024 report highlights the sheer scale of need presenting to homelessness services. 95% of accommodation providers and 100% of day centres supported clients with a mental health need, with high levels of substance misuse support, physical ill health, and dual diagnosis also common. Despite this, accessing the health and social care system remains challenging. Both accommodation providers and day centres (100% and 92% respectively) reported difficulties in accessing mental health services, nearly two-thirds had difficulties accessing drug and alcohol services, and over half reported difficulties accessing physical health services.

Homelessness is a health issue. While health services are under incredible pressure to support an ever-increasing number of people, the acute need for services for people experiencing homelessness must be considered as a core part of any inclusion health strategy and service development.

Our report highlights that homelessness providers are often the last line of defence for people who have fallen through the gaps of other public services including mental health, social care, and the justice system. This puts pressure on services, which are not set up to manage such high complexity of need and are already dealing with increased demand and constrained resources.

Breaking the cycle: funding and financial pressures

A driver for establishing this Review was to understand the impact of the 2008 loss of the Supporting People ringfence on the homelessness sector. Since then, we’ve tracked the sector’s primary funding sources to observe any changes and their resulting impact on service delivery.

We have seen a 2500% increase in Housing Benefit as the main funding source for accommodation providers and a 47% decrease in local authority commissioned contracts. The vast bulk of the Housing Benefit is in the form of Enhanced Housing Benefit funding exempt supported accommodation. This change has been massively transformative, impacting significantly on sector provision.

Notably, the last 17 years have seen a decrease in both low and high support needs services. These are disincentivised in the current funding model with the support element for high needs provision not covered through EHB and increasingly being cut from local authorities’ pressured budgets, and low needs providers struggling to justify their claims under strict HB rules. This has led to a more homogenous offer, ill-equipped to meet the increased complexity and diversity of people experiencing homelessness.

This funding model has also driven the increase in for-profit, bad actors within the supported accommodation sector, prompting the Supported Accommodation (Regulatory Oversight) Act and the incoming standards and licensing scheme. While the principle of national standards and a drive to improve accommodation quality is welcomed, there are concerns that the current proposals risk having enormous consequences on the sector.

2024 was a year of uncertainty and anxiety, as services up and down the country faced a funding cliff-edge, with the rollover of existing funding into 2025/26 not confirmed until December, and the looming challenge of increased National Insurance contributions. 67% of accommodation providers and 46% of day centres reported that the lack of inflationary increases in commissioned and grant funded projects leaves some services financially unviable. Nearly half of accommodation providers (48%) and day centres (46%) said increased financial pressures put their organisation at risk of service closures.

To break the cycle of crisis, we must flip the focus on to longer-term solutions centred on prevention and cross-government work. While the recent Comprehensive Spending Review gave a bit of a mixed bag here, we now look to the Homelessness Strategy as a critical opportunity to optimise the funding model to make this happen. Findings from the Support to End Homelessness series have informed our Breaking the Cycle Campaign and formed a key part of our joint campaign with Inside Housing.

A cross-government homelessness strategy

Support to End Homelessness 2024 highlights a system facing enormous, ongoing challenges and overwhelmed with rising demand and complexity of needs, as access to the wider health and social care system becomes increasingly difficult. Greater financial pressures and precarity, coupled with over-reliance on Housing Benefit as a primary funding source, are exposing systemic challenges in a sector vulnerable to outsized impact with future anticipated changes. The lack of sector growth despite rising demand highlights the fundamental issues at play.

Positively, regional variation reveals that local areas are working to reverse these trends, increase capacity and provide the effective support. However, a restructured funding system that can support a cross-government homelessness strategy will be essential if we are to make progress towards preventing and addressing homelessness across England.